From November 1st 2019, the eligibility criteria for VAT grouping were extended to allow individuals, partnerships, and Scottish partnerships to group with UK corporate bodies subject to certain conditions. Before the change, only corporate bodies such as Ltd companies or LLPs were eligible to form a VAT group.

The change of rules ensures that HMRC meet EU requirements by allowing unincorporated businesses to join a VAT group if the conditions are met. The main two conditions are:

- The unincorporated business must be entitled to register for VAT as a standalone business. It must be making or intending to make taxable supplies. Unlike corporate groups, a dormant entity cannot be included.

- The unincorporated business must control all of the corporate bodies in the group.

Unincorporated business can, therefore, benefit from Group VAT registration. Supplies of goods and services between group members are not subject to VAT, and each period will require only a single VAT return for the group.

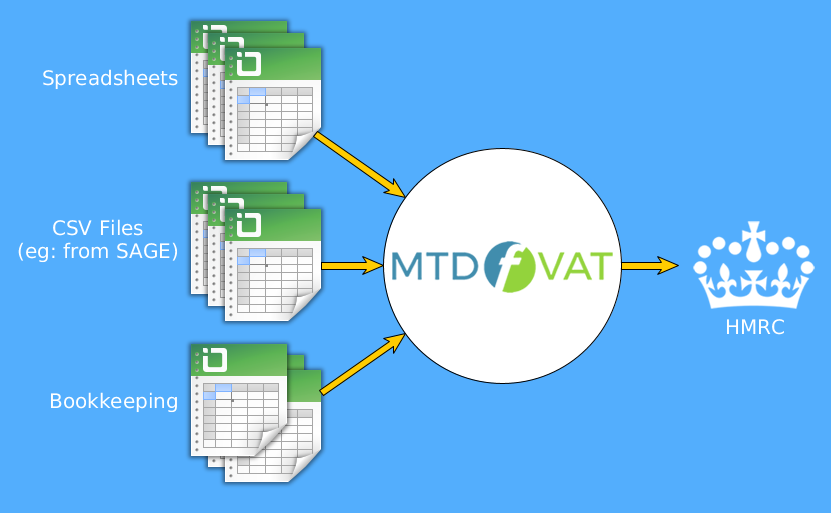

MTDfVAT’s Group VAT Feature

MTDfVAT now features a Group VAT functionality which allows you to build your VAT Return figures for the Group VAT Return within the software. It can handle exports from legacy sales and bookkeeping systems and allows easy submission of the VAT Return to HMRC directly within MTDfVAT.

To find out more about MTDfVAT, click here.

To get started with MTDfVAT, click here to choose your product version.

eligibility